When the idea of a 5G initiative first emerged there was talk in Europe of a big opportunity to take the lead and create another GSM-like success story. The 2nd generation mobile technology (GSM) had been a huge success. Europe led the world for best part of a decade not just in mobile technology but its service provision. The UK particularly excelled in the latter. The UK government liked the idea and set an ambition in 2015 for the country to become a leader in 5G. When 5G camed to be rolled out across the globe the UK is not even in the running in terms of leadership.

What went wrong?

The following analysis was submitted to DCMS in December 2021 to answer this question. It was submitted by the University of Surrey 5GIC in response to their call for evidence for their wireless infrastructure strategy.

Methodology: A generic model was constructed, shown in figure 2, comprising all the elements that need to come together for a country to successfully transition to a next generation mobile technology at scale. The model was then populated with the salient features that existed in the mobile network industry and market within two time slices thirty years apart. The first was the prevailing situation for the launch of 2G (GSM) and called Delivery Model 2.0. The second was the conditions prevailing for the launch of 5G and is called Delivery Model 5.0.

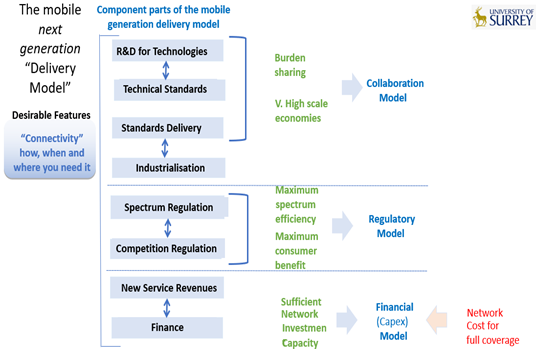

The generic mobile generation change model:

The basic delivery model comprises three sub-models. The collaborative model are all the things the industry do together cooperatively. R&D has always been well coupled with standardisation. Whilst industrialisation is competitive the mobile industry has this unique characteristic of moving together and this can be facilitated by a standards delivery action plan. Spectrum and competition regulation are coupled together. Finally, the business model has been simplified down to the financial Capex model of investment and return on investment (future revenues).

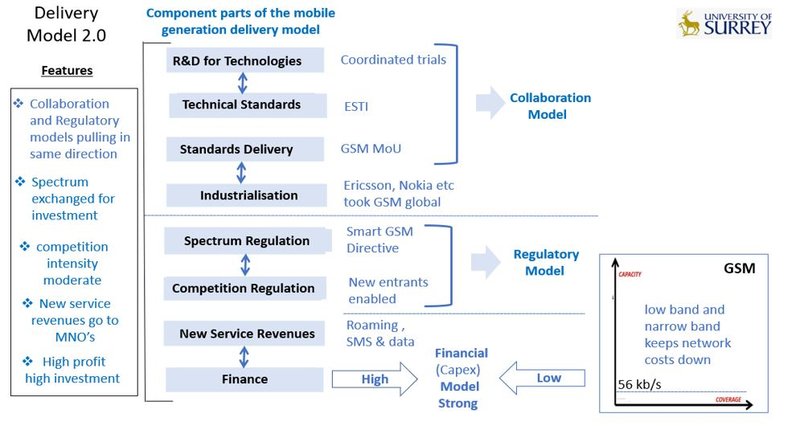

Delivery Model 2.0, shown in figure 3 below, is the model in Figure 2 but populated with factual elements that were in place for the roll out of 2G (GSM)

The three notable features of Delivery Model 2.0 are first, the collaboration model and regulatory model pulling in the same direction (by design). The UK and EU Commission played pivotal roles in this. Second, the mobile network investment cost for national coverage is relatively low. Third the new revenues resulting from the investment all flow to the mobile operator who is making the investment. The result is a high profit-high investment capacity delivery model.

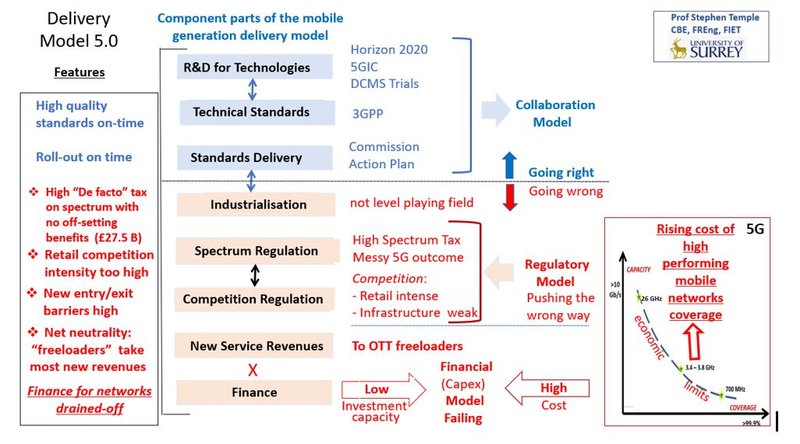

Delivery Model 5.0 shown below in figure 4 is the model in Figure 2 but populated with factual elements that are in place today for the roll out of 5G

The changes on both sides of the financial balance sheet have been happening in plain sight over a number of years. The unique contribution of this analysis is bringing into much clearer focus the cumulative impact of the concurrent changes to the point of passing a tipping point in respect of sufficient investment capacity in the UK to roll out 5G at scale.

The three notable features of today’s delivery model are:

The financial model in Delivery Model 5.0 has become inverted relative to Delivery Model 2.0 on both sides of the balance sheet. The outcome is today’s low investment capacity to meet the ambition the government of 2015 set for the UK to be a leader in 5G.

The term “freeloader” may seem an unduly emotive term to use. It is technically the right term, as the definition of a “freeloader” is an entity benefiting from something without contributing to its cost. But its use is helpful in drawing attention to the fact that all the regulatory measures have been for Ofcom’s view of “good causes” whether it is low prices for consumers, “free carriage” for new Internet services or “de facto” raising of taxes for the Treasury through spectrum auctions and fees. The regulator has been a success in delivering on those causes but has had a profound negative impact on the government’s goal of the UK becoming a leader in 5G. It is also contributing to a massive cost squeeze on the traditional supply industry. In the past, the lion’s share of research for a mobile next generation technology has come from the large system vendors. If their revenues continue to be squeezed, then their capacity to invest in long term research will inevitably get squeezed with it.

Read more

The pressing need across Europe is for pro-investment mobile regulation. This book describes, for the first time, what a pro-investment mobile regulatory framework might look like.

Casting the Nets provides an unparalleled insight into the great digital transformation of Britain’s communications networks over the period 1984-2004. It gives a graphic description of industrial policy-in-action and brings to life what is involved.

The most authoratative history of digital mobile phones, from the first ideas jotted down on paper to the global phenonemon it is today, is meticulously detailed on this web site.

All content here (c) copyright of Stephen Temple